Buying your first home is exciting, but it can also be a little nerve-wrecking because it’s something you’ve never done before.

]]>Buying your first home is exciting, but it can also be a little nerve-wrecking because it’s something you’ve never done before. And trying to think of everything you need to do can feel like a lot. But here’s the key.

You don’t have to figure everything out on your own. And you don’t have to do it all at once. Just tackle it one thing at a time.

Here’s a simple list of 3 main things you should focus on to help you get started.

1. Assemble Your Team: Don’t Do This Alone

Buying a home is a team sport. And having the right professionals by your side can make a world of difference. Here’s who you need to find:

- A local real estate agent is your guide from the first showing to closing day. They’ll make sure you understand all the details along the way, so you feel confident in your decision.

- A trusted lender will walk you through loan options, monthly payments, and what’s realistic for your situation. That information is something you’re going to want early on.

2. Prep Your Finances: Set the Foundation First

This is what determines what you can afford, how competitive you’ll be, and how confident you’ll feel when it’s time to make an offer. Here’s how to get ready:

- Check your credit score. Your credit score impacts the loan options you’ll qualify for and even the mortgage rate you’ll get. Knowing this number early gives you time to work on raising your score, if you want to.

- Save for your down payment and closing costs. Most buyers focus on the down payment, but closing costs matter too. Having savings set aside for both helps you avoid last-minute stress and surprises.

- Look into assistance programs. Many first-time buyers qualify for programs that’ll give their homebuying savings a boost. This can make buying possible sooner than you expect.

- Talk to a lender about mortgage options. Fixed-rate, adjustable-rate, FHA, VA, and conventional loans all work differently. Understanding the options helps you choose what fits your goals best.

- Get pre-approved. A pre-approval tells you what a lender would be willing to give you for your home loan. This’ll help you figure out your price range and set you up to move fast when the right home comes along.

- Figure out your budget. Your mortgage is just one part of homeownership. Budgeting for your utilities, home insurance, and everyday expenses and maintenance will help make sure your payment feels comfortable, not stressful.

3. Gather Your Documents: Save Time (and Stress)

When you’re officially ready to kick off the buying process, lenders are going to need to verify your income, assets, and financial history. Having these documents ready-to-go upfront can speed up the process and reduce back-and-forth. Here’s what Bankrate says you need to prep:

- W-2s and tax documents (past 2 years). These show income stability and help

- Recent pay stubs (generally the past 1–2 months). Pay stubs confirm your current income and employment status.

- Bank statements (past 2–3 months). These show your savings, spending patterns, and where your down payment funds are coming from.

- Investment account statements (past 2-3 months). If you’re using investments as part of your financial picture, lenders may ask for these as well.

- Copy of your driver’s license. This verifies your identity and is required for loan processing.

- Residential history (past 2 years). Lenders use this to confirm stability and background information.

- Statements for any outstanding debts (past 2 months). Student loans, auto loans, and credit cards affect your debt-to-income ratio, so lenders will want to know about them.

- Proof of supplemental income. Bonuses, commissions, side work, or child support may count toward your income if documented properly.

Note: the exact time frames and list of documents may vary lender to lender. This is just a general rule of thumb to help you get the ball rolling.

Bottom Line

Buying your first home doesn’t mean you have to have everything figured out. It just requires a plan.

If you start with your finances, organize your documents, and surround yourself with the right people, you’ll be in great shape when the time comes to make a move.

And if you want more information on anything in this list or just need help getting started, reach out to an agent.

]]>You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017.

]]>You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

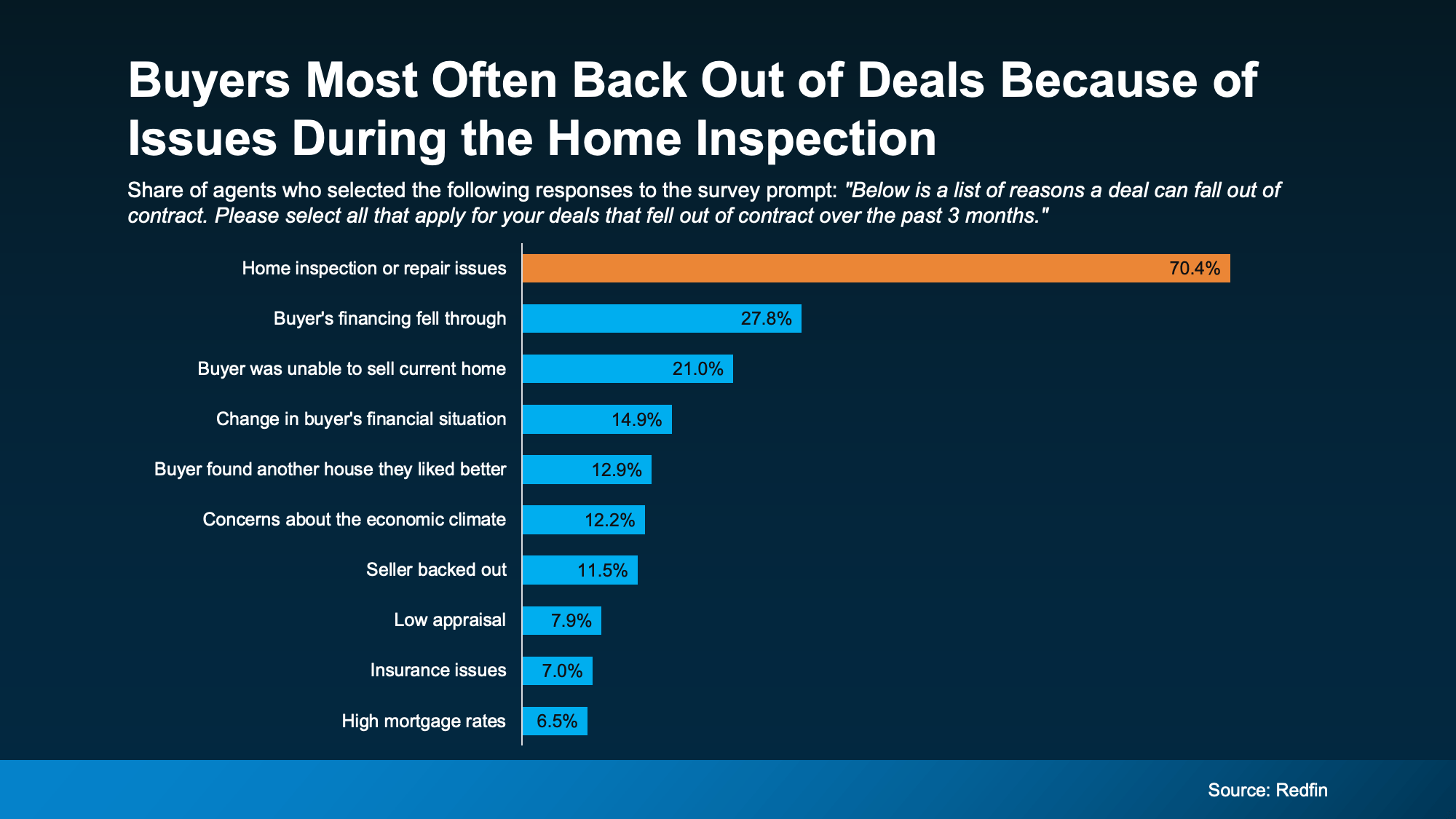

The Top Dealbreaker: Issues That Pop Up During the Inspection

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

Why Fixing Things Before You List Matters More Today

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

How Your Agent Can Help Give You the Edge

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They'll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

- Roof leaks or damage: sagging, leaking, etc.

- Plumbing problems: standing water, leaks, water damage, etc.

- Electrical concerns: outdated or exposed wiring, missing GFCI outlets, etc.

- HVAC issues: non-functioning units

- Pest or insect damage: termite colonies, etc.

- Hazardous materials: lead, mold, asbestos, etc.

- Safety/code violations: missing smoke detectors, windows stuck closed, etc.

- Structural problems: cracks in the foundation, sagging floors, etc.

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

The Benefits of a Pre-Listing Inspection

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

- Fix concerns before you list, or disclose issues upfront

- Avoid having to respond or negotiate under pressure

- Stop scrambling to find contractors with availability before your closing date

But remember, you don't have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

- Decide if a pre-listing inspection is worth it where you live

- Recommend a trusted inspector (if you decide to get one)

- Look at the results with you to identify true dealbreakers in your market

- Help you decide what to fix or what to credit

- Make sure you avoid over-spending or under-preparing

Bottom Line

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, connect with an agent.

]]>Foreclosures are ticking up. And that may make your mind jump straight to thoughts of 2008 – specifically to what happened to the market during the housing crash.

]]>Foreclosures are ticking up. And that may make your mind jump straight to thoughts of 2008 – specifically to what happened to the market during the housing crash. So, let’s do exactly what your brain already wants to do, and see if there’s any connection there.

The simple truth is foreclosure filings are rising. But they’re nowhere near crisis levels. And that’s not where they’re headed either. Here’s why.

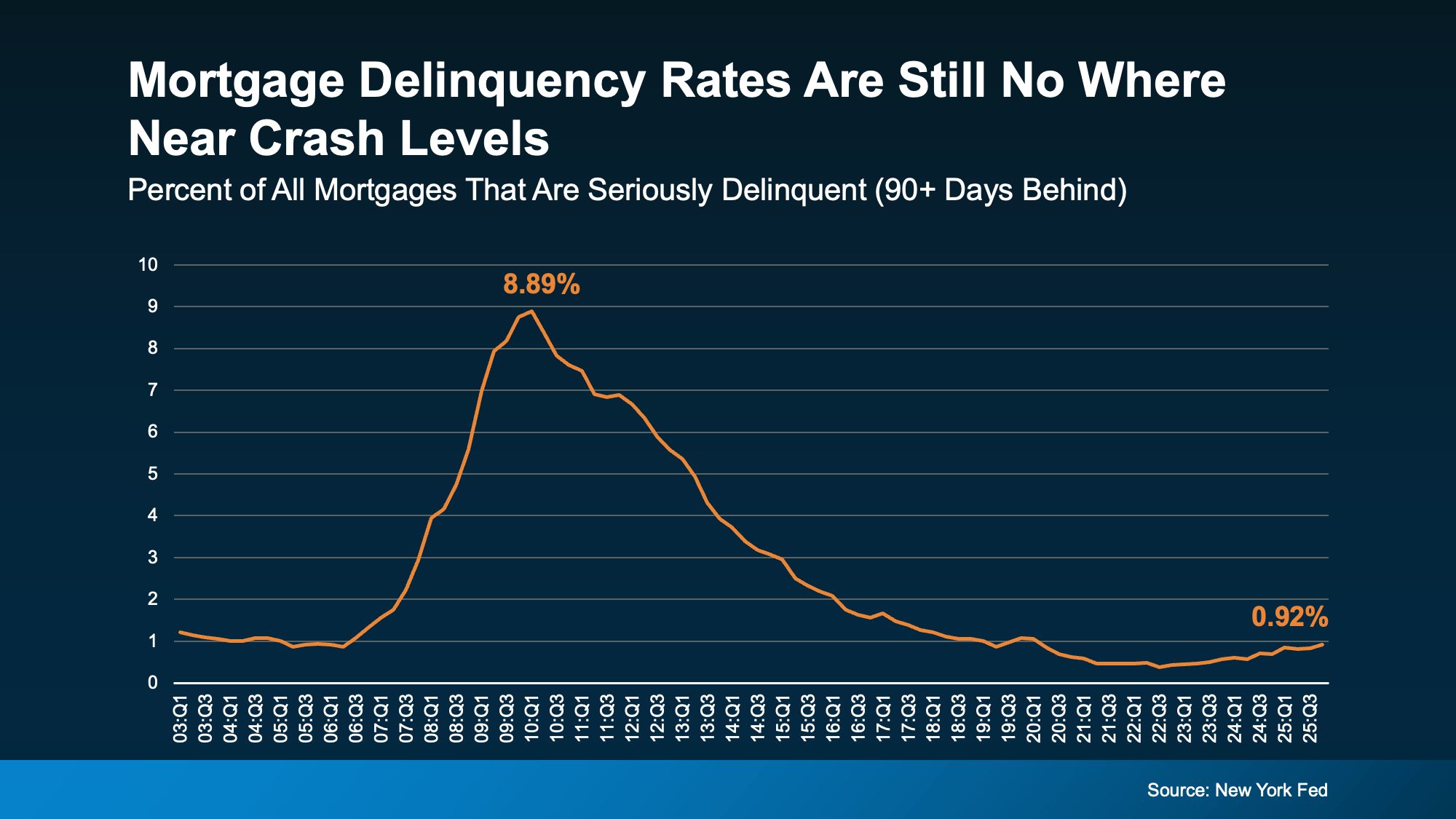

Take a look at serious delinquencies – loans where the homeowner is more than 90 days late on their mortgage payments.

While those have increased slightly, data from the New York Fed shows they still remain low. And they aren’t anywhere close to levels seen when the market crashed (see graph below):

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

Right now, about 1% of mortgages are seriously delinquent. That’s only 1 in 100.

In the years around the crash, they were up around 9%. That’s 1 in 11.

That’s a big difference.

And it’s important to remember not all delinquencies even become foreclosure filings. Some homeowners who are falling behind will work out repayment plans with their banks and lenders because banks don’t want to see a wave of foreclosures either.

That’s why foreclosure numbers are even lower than delinquencies. ATTOM shows only 0.3% of all homes are currently going through a foreclosure filing. And those won’t even all go to a full foreclosure. That’s not a wave. That’s a ripple at most.

If People Are Falling Behind on Payments, Why Aren’t There Even More Foreclosures?

And maybe you’re wondering, if people are struggling financially, why aren’t there more foreclosures? Here’s the easiest way to answer that.

When households feel financial pressure, they tend to prioritize their mortgage payment above almost everything else. Because the last thing they want to lose is their home.

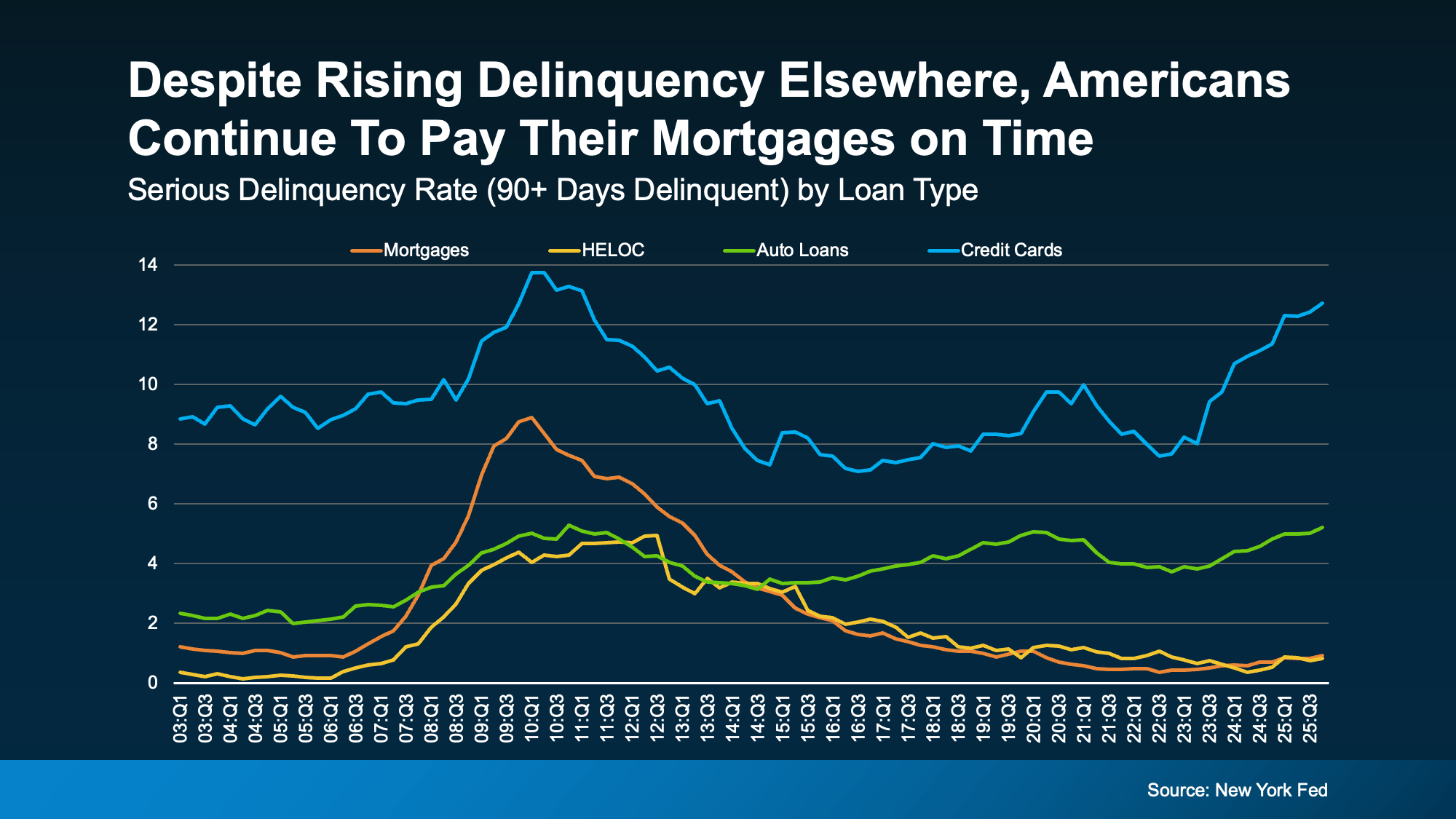

Data from the New York Fed shows serious delinquencies have risen more for credit cards and auto loans (the blue and green lines). But mortgage delinquencies and home equity lines of credit (borrowing against the value of your home) aren’t seeing the same big uptick (the yellow and orange lines). They’re a lot more stable overall.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

Home Equity Changes Everything

Many people have built significant equity over the past several years. And that creates options. As Daren Blomquist, VP of Market Economics at Auction.com, explains:

“Distressed homeowners… many times they still have equity in their homes. There’s an opportunity for them to sell that home, avoid foreclosure, and walk away with equity.”

That’s a major difference from 2008. Back then, many homeowners owed more than their homes were worth. And selling wasn’t an easy solution. Today, for many people, it is. And even in situations where equity isn’t enough, homeowners are encouraged to contact their loan servicer early to explore alternatives to foreclosure.

Bottom Line

Are foreclosure filings rising slightly? Yes. Are they anywhere near crash territory? No. And homeowners today have far more equity and flexibility than they did during the crash.

If you’re concerned about what you’re seeing in the headlines, the best move isn’t panic, it’s perspective. And the data right now says this isn’t 2008 all over again.

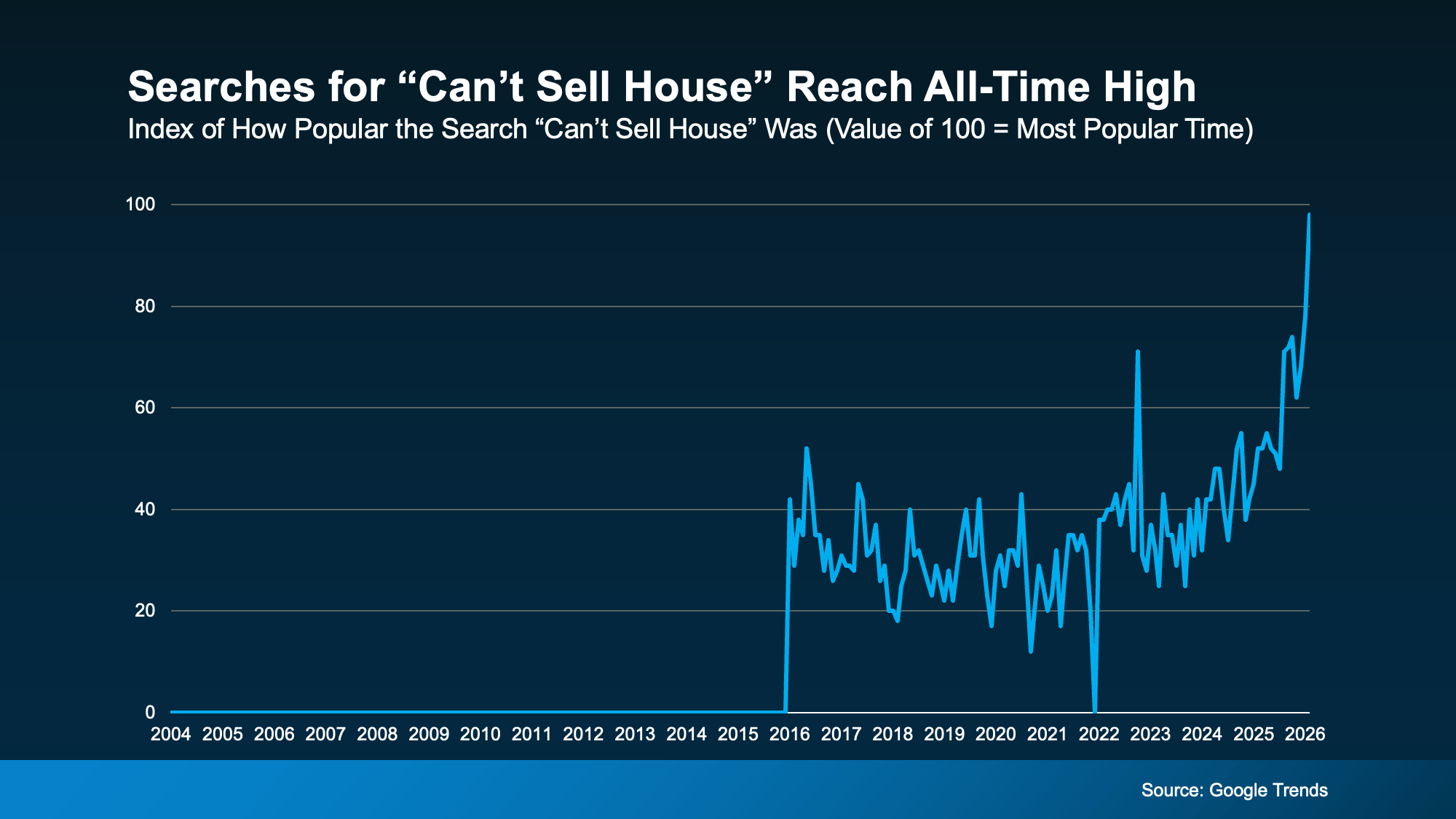

]]>Online searches for “can’t sell house” just hit an all-time high according to Google Trends.

]]>Online searches for “can’t sell house” just hit an all-time high according to Google Trends. So, if your house has been sitting on the market without any bites, you’re not the only one. But it's also not the end of the road.

Homes are selling every day, so you can turn this around. You just need to take another look at your approach.

If you’re feeling this pain, know this: an online search engine isn’t where you should go for your answers. It’s much better to talk to your agent. Because a search engine doesn’t know your market or your house. But your agent does.

If you’re feeling this pain, know this: an online search engine isn’t where you should go for your answers. It’s much better to talk to your agent. Because a search engine doesn’t know your market or your house. But your agent does.

While a quick search or an AI platform may give you some tips on what to try, only an expert agent can actually diagnosis what’s going on – and how to fix it.

For example, your agent knows most homes that struggle to sell today are usually being held back by one (or more) of these three things.

1. Presentation: Buyers Will Compare Everything

When inventory was tight a few years ago, buyers overlooked imperfections because they had to, or they’d lose out to another bidder. Now? That’s no longer the case.

Today’s buyers scroll through dozens of listings in just minutes. They compare condition, updates, lighting, finishes, layout, and more – all side by side. If your home feels dated, cluttered, or in need of repairs, buyers will notice and it’ll knock your house right off their list of contenders.

This doesn’t mean you need a full renovation. But it does mean first impressions matter again. To compete today, you need curb appeal. Clean spaces. Neutral colors. Professional photos. If there are scuffs on the walls, obvious repairs, or too many outdated features, it could be what’s holding you back.

2. Pricing: If the Price Isn’t Compelling, It’s Not Selling

This is maybe the hardest one to hear, but what your neighbor sold their house for a few years ago isn’t necessarily the same price you’ll get today. As Selma Hepp, Chief Economist at Cotality, says:

“For sellers, the days of pricing aggressively and expecting instant offers are largely over. Homes that are well-priced and well-presented will still sell, but pricing discipline matters more than it did during boom years.”

Buyers are budget-conscious right now. If your home is priced based on outdated expectations instead of current demand, buyers may still look at your house online… but they likely won’t write an offer. Or, they’ll make an offer that you think is too low.

Pricing too high for this market is one of the top things sellers miss the mark on today. And those who aren’t willing to meet the market where it is or entertain offers may feel stuck.

3. Access: If Buyers Can’t See It, They Can’t Buy It

It sounds obvious but limited showing availability can kill your momentum. If your house isn’t easy to see because you’re restricting showings to evenings only, no weekends, or requiring a 24-hour notice, you're cutting your buyer pool down by more than you may realize.

And the more friction you create, the fewer buyers walk through the door.

In a market where buyers have more options, the last thing you want to do is give them a reason to skip your house. Availability matters because if no one sees it, no one buys it.

Don’t Let Search Results Decide Your Next Step

When your house isn’t selling, it’s tempting to spiral and wonder if it’s the market or if something’s wrong with your house. But instead of searching for answers online, here's what to do.

Sit down with your agent and ask three honest questions:

- What are buyers looking for in today’s market?

- What feedback are we getting from showings?

- Why do you think my house hasn’t sold yet?

That conversation will bring a lot more clarity than any search engine results.

Bottom Line

If your listing feels stuck, it’s not a sign you shouldn’t sell. It’s the market giving you feedback. And feedback is powerful when you use it.

Start with a real conversation with a real agent about what’s working and what’s not. Your agent will be able to tell you which small adjustments could totally change the momentum. Because in this market, the sellers who adapt are the ones who move.

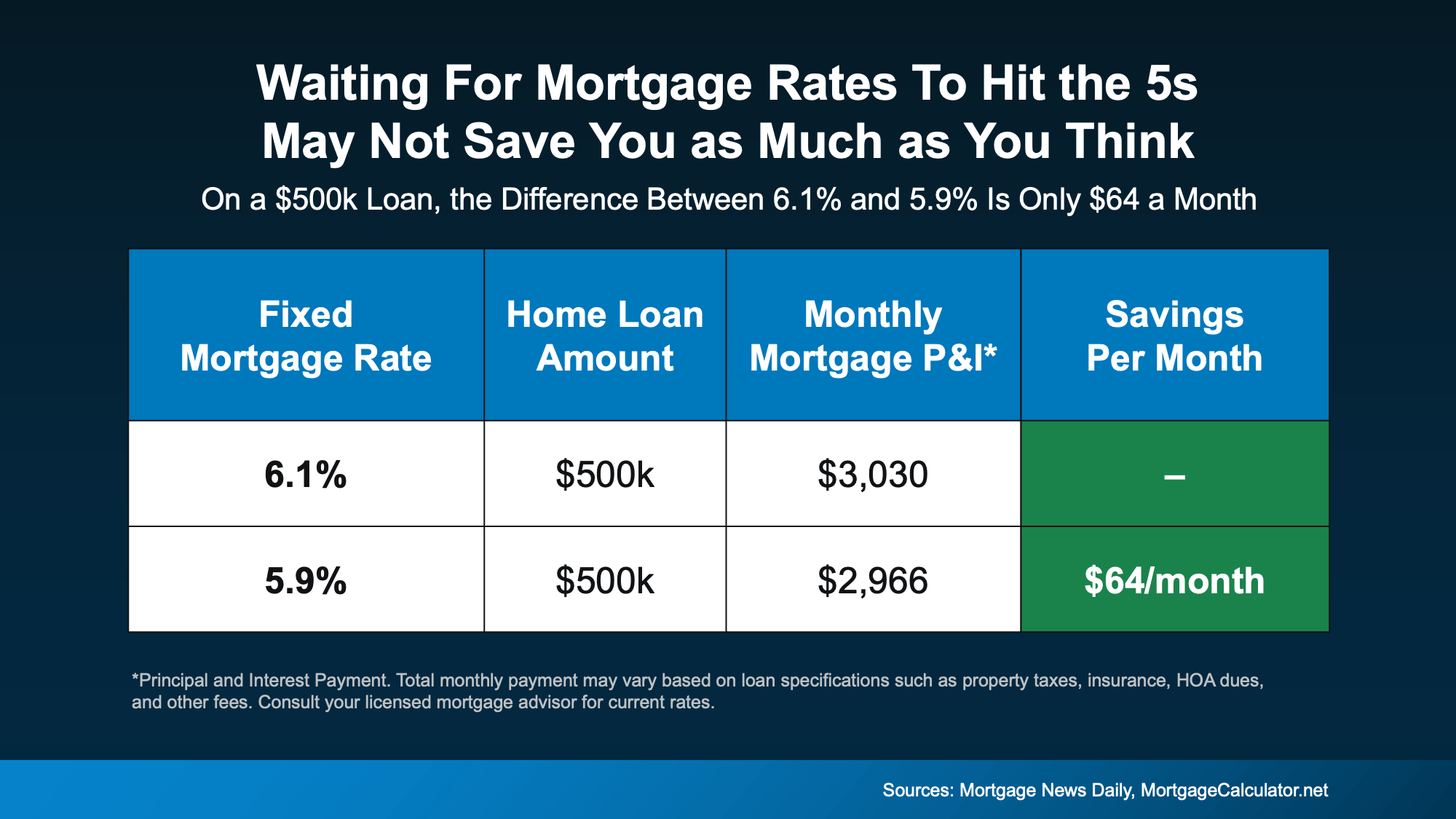

]]>Mortgage rates have already dropped into the upper 5s twice this year. But after just a few days, they ticked back up into the low 6% range.

]]>Mortgage rates have already dropped into the upper 5s twice this year. But after just a few days, they ticked back up into the low 6% range. If you saw that and thought, “Great. I missed it,” you’re not the only one.

A lot of buyers are treating the 5s like some kind of magic number. As if moving from 6.1% to 5.99% suddenly changes everything. And from a mindset perspective, it does feel different.

But here’s the part most people don’t actually run the math on.

The Payment Difference Isn’t What You Think

Let’s say you’re looking at a $500,000 home loan. At 6.1%, generally speaking, your principal and interest payment is roughly $3,030 per month. At 5.9%, it’s about $2,966 per month.

That’s a difference of only $64 a month.

Not $300.

Not $500.

Sixty dollars.

Let that sink in for just a moment.

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

The psychological impact of seeing a 5 in front of your rate can feel big. The financial impact? It might be something you don’t even notice when it’s all said and done.

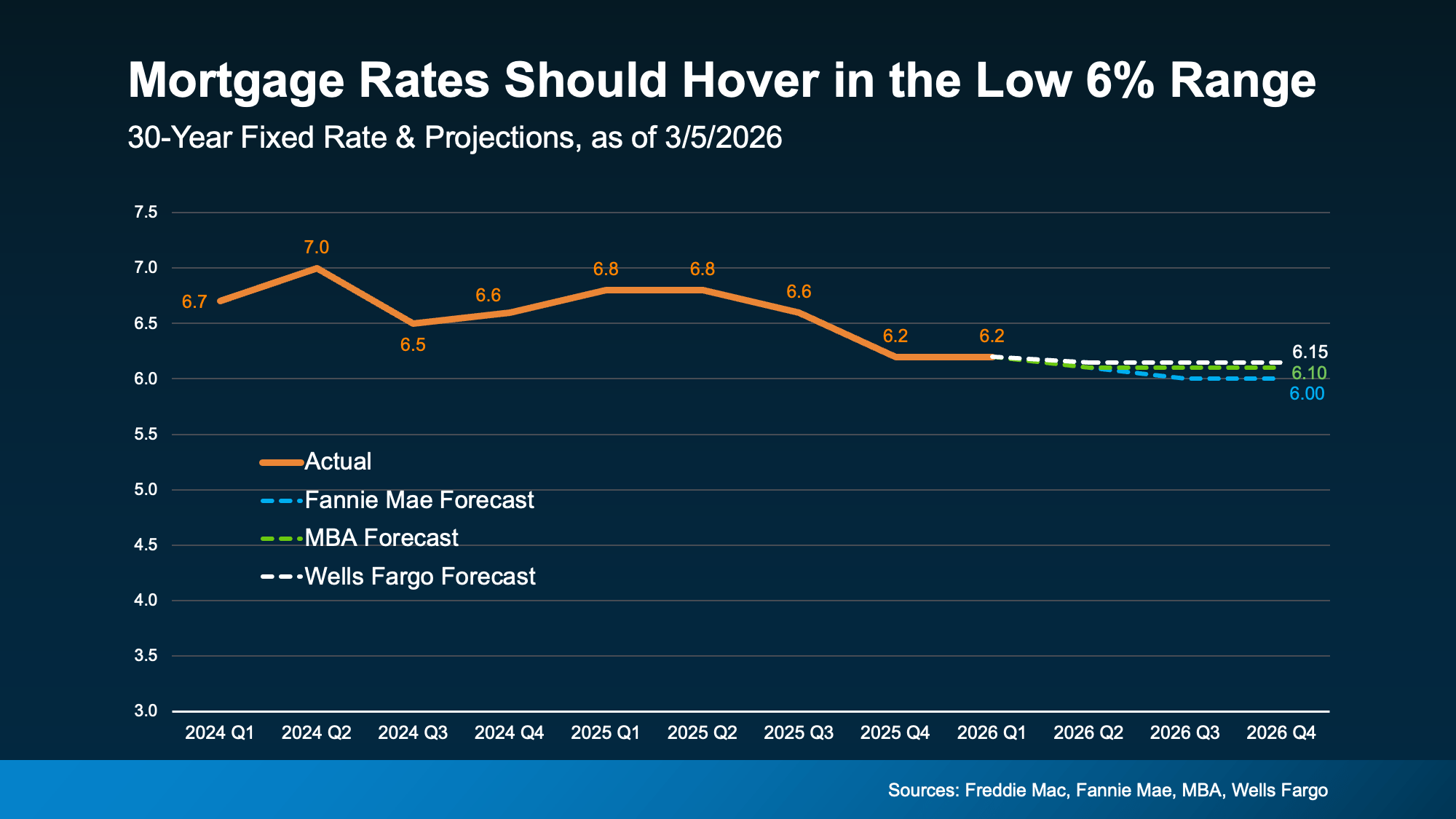

Experts Aren’t Predicting a Big Drop

Another important piece to think about: most housing economists aren’t forecasting a long-term return to 5% territory anytime soon.

While rates will move up and down, likely hitting the high 5s here and there, the broader expectation is for mortgage rates to hover in the low 6% range this year, not stay in the 5’s or decline much more.

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

The Bigger Question to Ask

Instead of asking, “Did I miss the 5s?” A better question is: “Does today’s payment work for me?”

If the monthly payment fits comfortably in your budget, and you’ve found a home that meets your needs, the difference between 6.1% and 5.9% likely isn’t the deciding factor. It might be one of them, but it shouldn’t be everything.

And remember, mortgage rates aren’t permanent. If they drop meaningfully later, refinancing is always an option. But you can’t refinance a home you didn’t buy.

Waiting Might Feel Safe, But It Isn’t Always Strategic

It’s natural to want the best possible rate. Everyone does. But sometimes buyers overestimate how much a rate in the high 5s will change things in today’s market.

Don’t miss the fact that rates have already come down. A year ago, they were in the 7s. Now? They’re hovering in the low 6s. And for a lot of people, that percentage point difference that’s already here is the real game changer.

If you paused your plans when rates were higher, now may be the right time to re-run your numbers. Not because rates are “perfect.” But because the monthly payment math might work better than you think, even with rates in the low 6s.

Before assuming you’ve missed your moment, take another look at the numbers.

You may find it never disappeared.

Bottom Line

If you’ve been sitting on the sidelines waiting for that magic five number for rates, that strategy may not pay off as much as you’d expect.

Connect with an agent or lender so you can double check the math at your price point. You may realize payments are already within your range.

]]>Homeowners looking to sell usually want three things: plenty of interested buyers, strong offers, and a short timeline. Spring is the season that most often delivers all three.

]]>Homeowners looking to sell usually want three things: plenty of interested buyers, strong offers, and a short timeline. Spring is the season that most often delivers all three.

So, if a move has been on your mind this year, this is the window where momentum tends to work in your favor. Here’s what makes this season so powerful for sellers.

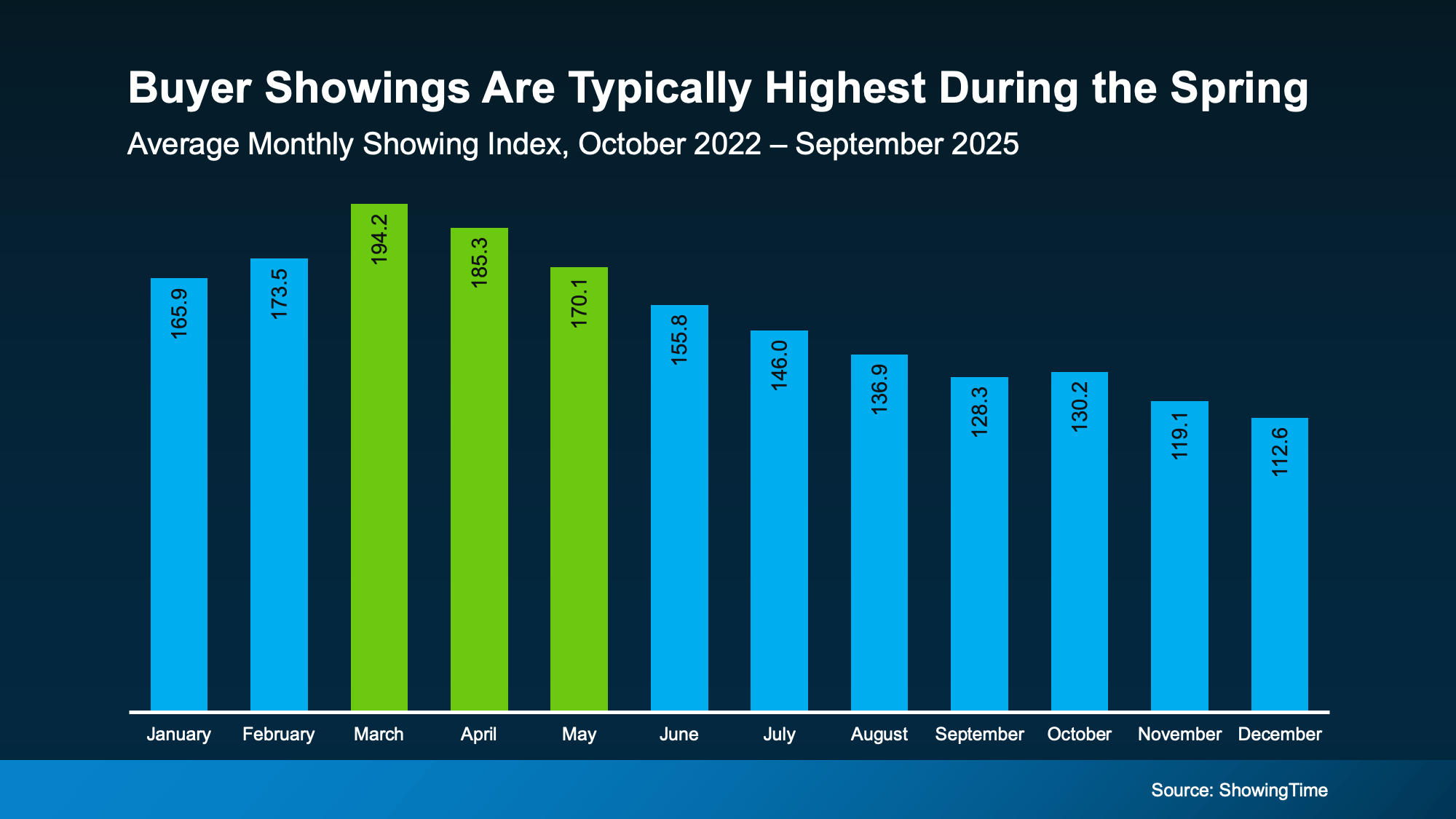

1. More Buyers Will Be Looking

Typically speaking, in the housing market, there’s no more popular time to move than the Spring. Historically, data coming out of ShowingTime proves that’s when buyer activity peaks each year. Take a look for yourself (see graph below):

And this year, there’s more than just the seasonal trend working in your favor. Mortgage rates are also sitting near 3-year lows – and that combination matters.

And this year, there’s more than just the seasonal trend working in your favor. Mortgage rates are also sitting near 3-year lows – and that combination matters.

More buyers + improving affordability = more eyes on your house.

That doesn’t mean the market will return to the frenzy of the pandemic – far from it. But it does mean more buyers will be ready to re-enter the market. And that’s good for you. As Redfin says:

“Homebuying demand is improving . . . and mortgage-purchase applications are sitting near their highest level in three years. . ."

You should make sure your house is listed so you can take advantage of the uptick in demand. Because more activity means one thing: more opportunity to get a deal done.

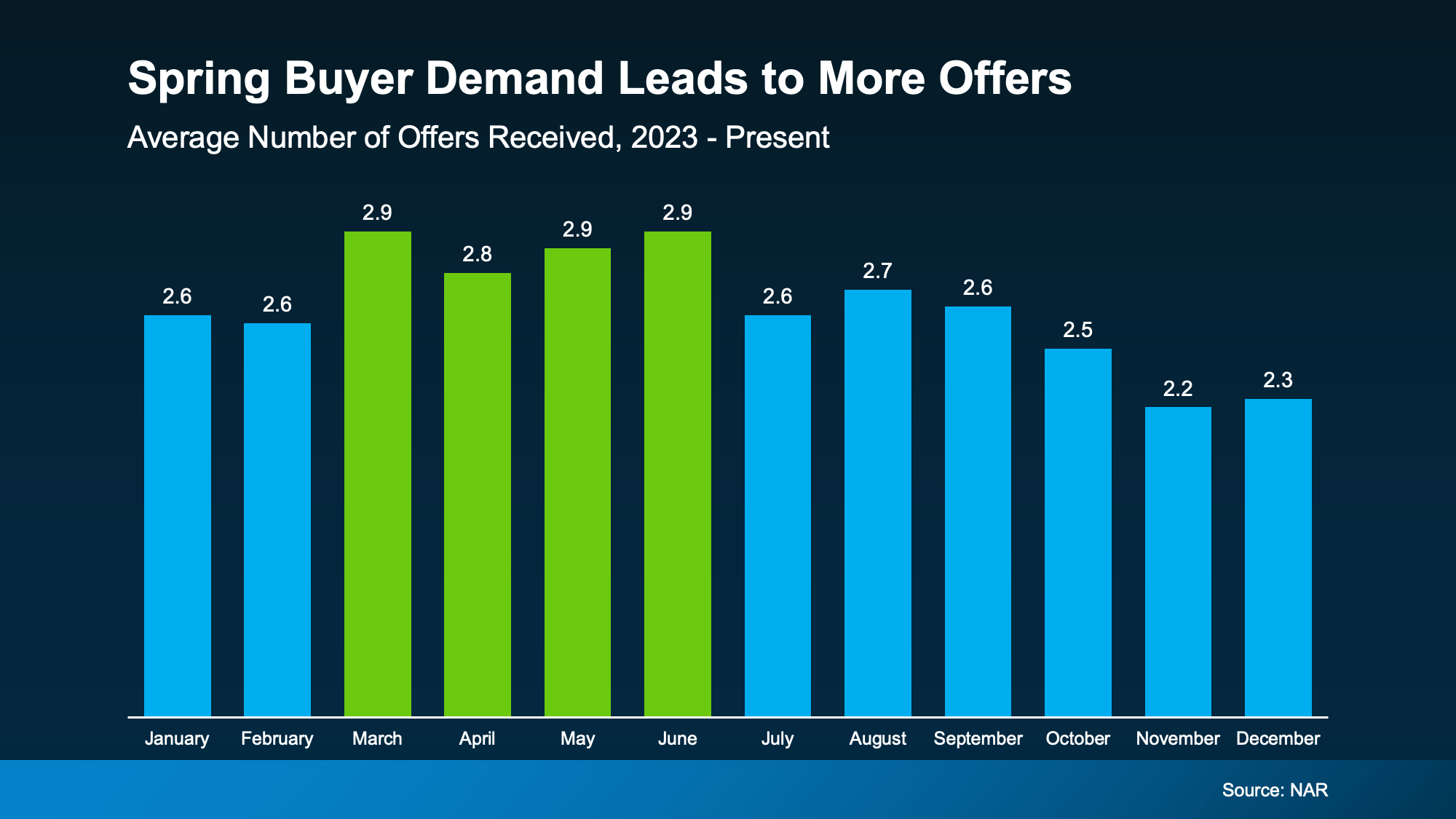

2. You May Get More Offers

With more buyer demand, it makes sense that you may get more offers on your house. And history shows that’s usually true.

If we look at the data for the last three years from the National Association of Realtors (NAR), and take the averages for each month, it’s clear sellers in the Spring get more offers (see graph below):

Now, don’t expect the excessive bidding wars that were so famous in 2020 and 2021. But it does mean, seasonality could help you out this Spring. As Realtor.com explains:

Now, don’t expect the excessive bidding wars that were so famous in 2020 and 2021. But it does mean, seasonality could help you out this Spring. As Realtor.com explains:

“Spring typically brings out more buyers who are ready to make a move before summer. Listings see more views, showings, and offers during this season.”

And that could be really good for your bottom line.

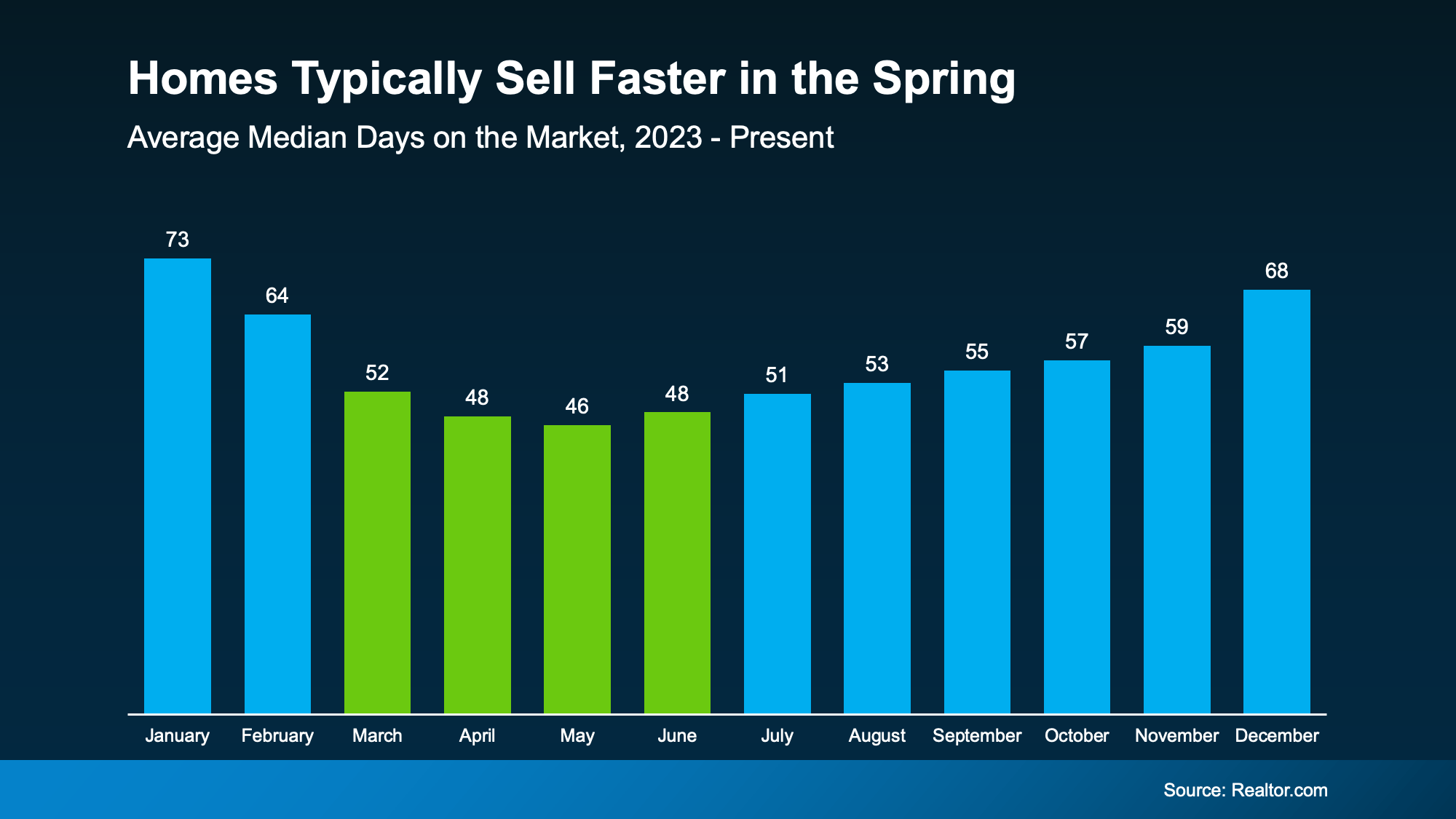

3. Homes Usually Sell Faster

There’s one more predictable pattern that happens pretty much every Spring based on research from Realtor.com. Homes sell faster (see graph below):

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that's a difference you can feel.

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that's a difference you can feel.

Since homes have been taking longer to sell lately, listing your house during what’s usually the most active time of the year means you’re setting yourself up to move as quickly as possible. And isn’t that what sellers really want?

The faster your home sells, the earlier you can move on to what’s next for you.

If you’re eager to go on to your next chapter, need to downsize, or you’ve run out of space, Spring may be your best time to sell.

Bottom Line

Spring doesn’t guarantee a sale. Strategy still matters. But this season gives you something valuable: momentum.

More buyers. More activity. More opportunity.

The real question is: if you’re going to sell this year, why not do it when the odds are in your favor?

Talk to an agent about what selling this season could mean for your house and your timeline.

]]>You’ve probably seen posts on social media talking about how “home prices are falling.”

]]>You’ve probably seen posts on social media talking about how “home prices are falling.” And when you see something like that, it’s normal to wonder:

Is this the start of a crash?

What does this mean for my house?

Let’s clear this up right away. This is not a crash. And your home is not suddenly losing a lot of value.

The National Story – Prices Are Still Going Up

Here’s what often gets left out of what you’re seeing online. While some markets are experiencing slight declines, they’re the minority. Most places are still seeing prices rise or at the very least, hold steady.

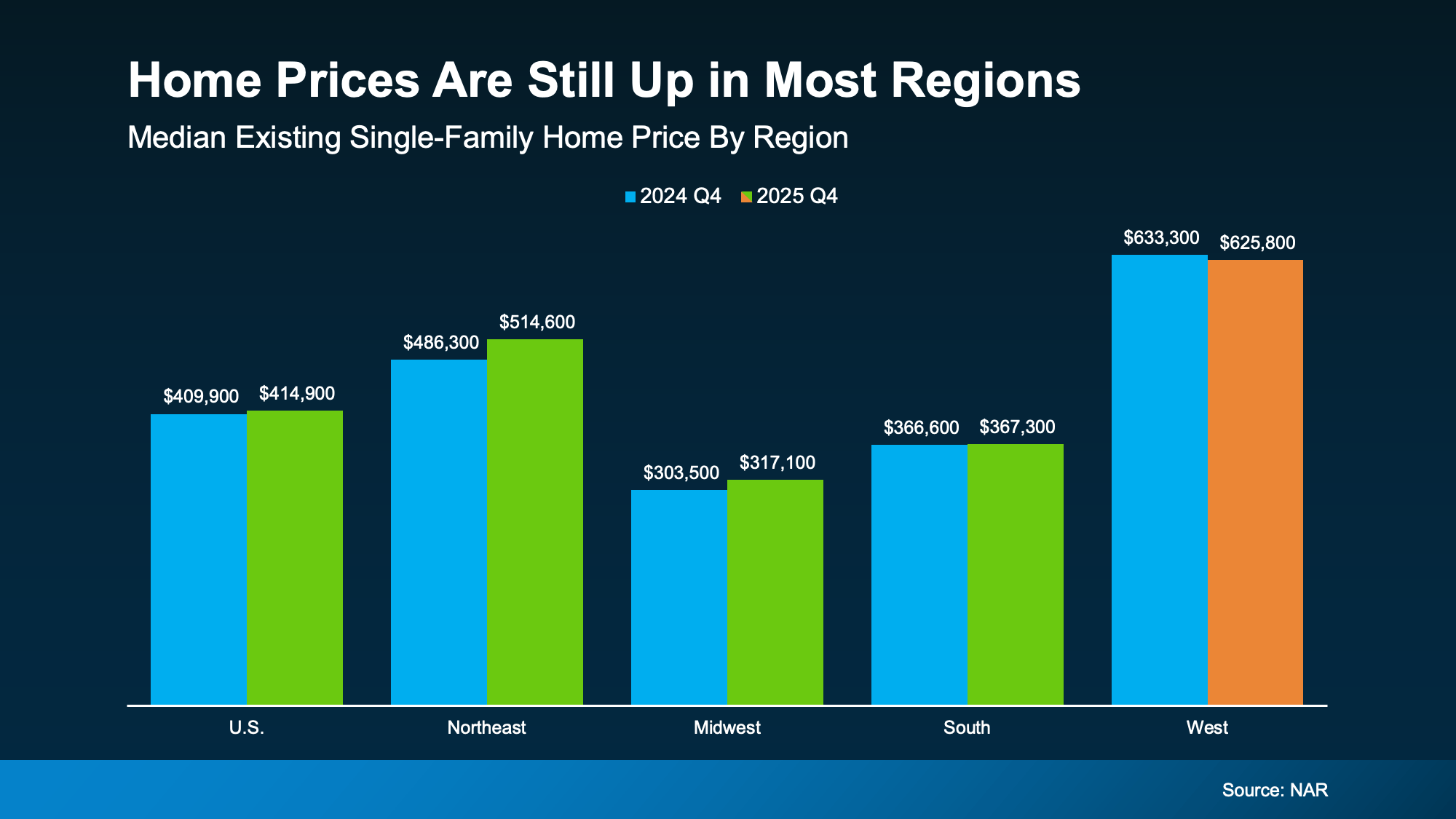

That’s why, at the national level, home prices are still rising, just at a slower pace. According to the National Association of Realtors (NAR):

“Home prices continued to rise in the fourth quarter of 2025. National median prices rose 1.2% year over year to $414,900.”

That’s not the rapid growth of a few years ago, but it’s not a downturn either. And just to really drive this home, here’s a look at the data from NAR at a regional level, so you can see that the negative narrative spun up online isn’t the whole truth (see graph below):

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

Home prices are up (or at least holding steady) in the Northeast, Midwest, and South. The West has seen some small declines in certain markets, but “small” is the key word.

There is no wave of falling prices across the country. Instead, there are just a few pockets adjusting after several years of what’s typically considered unsustainable or exponential growth.

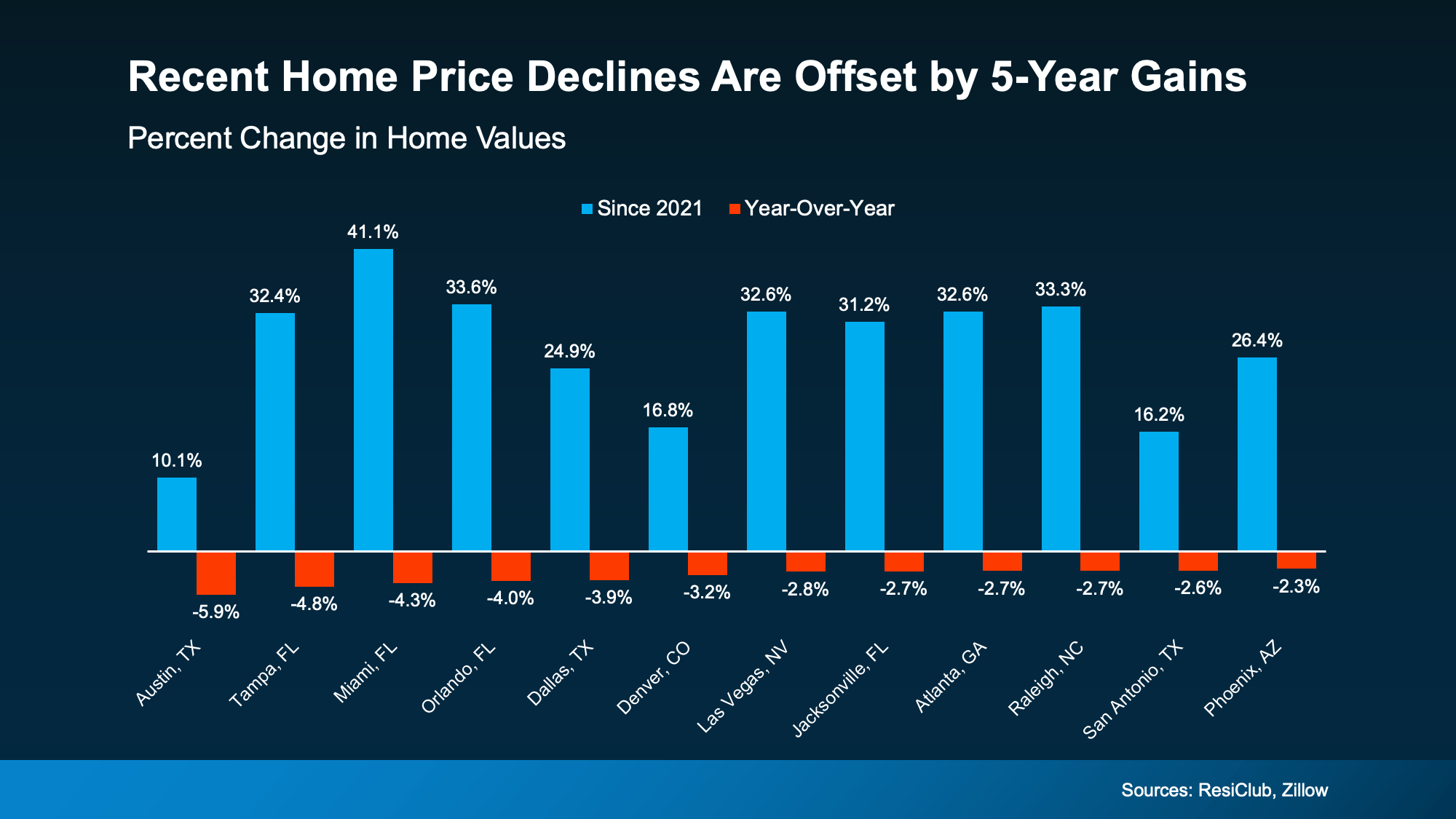

Yes, Some Markets Have Come Down, But Look at the Bigger Picture.

Okay, but what about the places where prices have declined? According to ResiClub and Zillow, that’s not a cause for major concern. When you zoom out and look at those same markets over the past five years, the story changes (see graph below):

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

In the areas with recent declines, home values are still significantly higher than they were just five years ago. That’s a direct reflection of how much home values have gone up.

Online chatter tends to shine a spotlight on the few areas that are down. But the bigger picture shows most homeowners are still in a very strong position.

Of course, every market, and every home, is different. But broadly speaking, home values are holding steady. And this isn’t a sign of widespread trouble in the market.

Bottom Line

Despite what you may be seeing online, home prices are rising or holding steady in most parts of the country.

If you’re curious what your home is worth today, take a look at the numbers with a local real estate agent. Because context, and local expertise, matter more than what you’re seeing online.

]]>What if you didn’t have a mortgage payment on your next house? It may sound a little unrealistic. But for a number of homeowners, it’s actually doable.

]]>What if you didn’t have a mortgage payment on your next house? It may sound a little unrealistic. But for a number of homeowners, it’s actually doable.

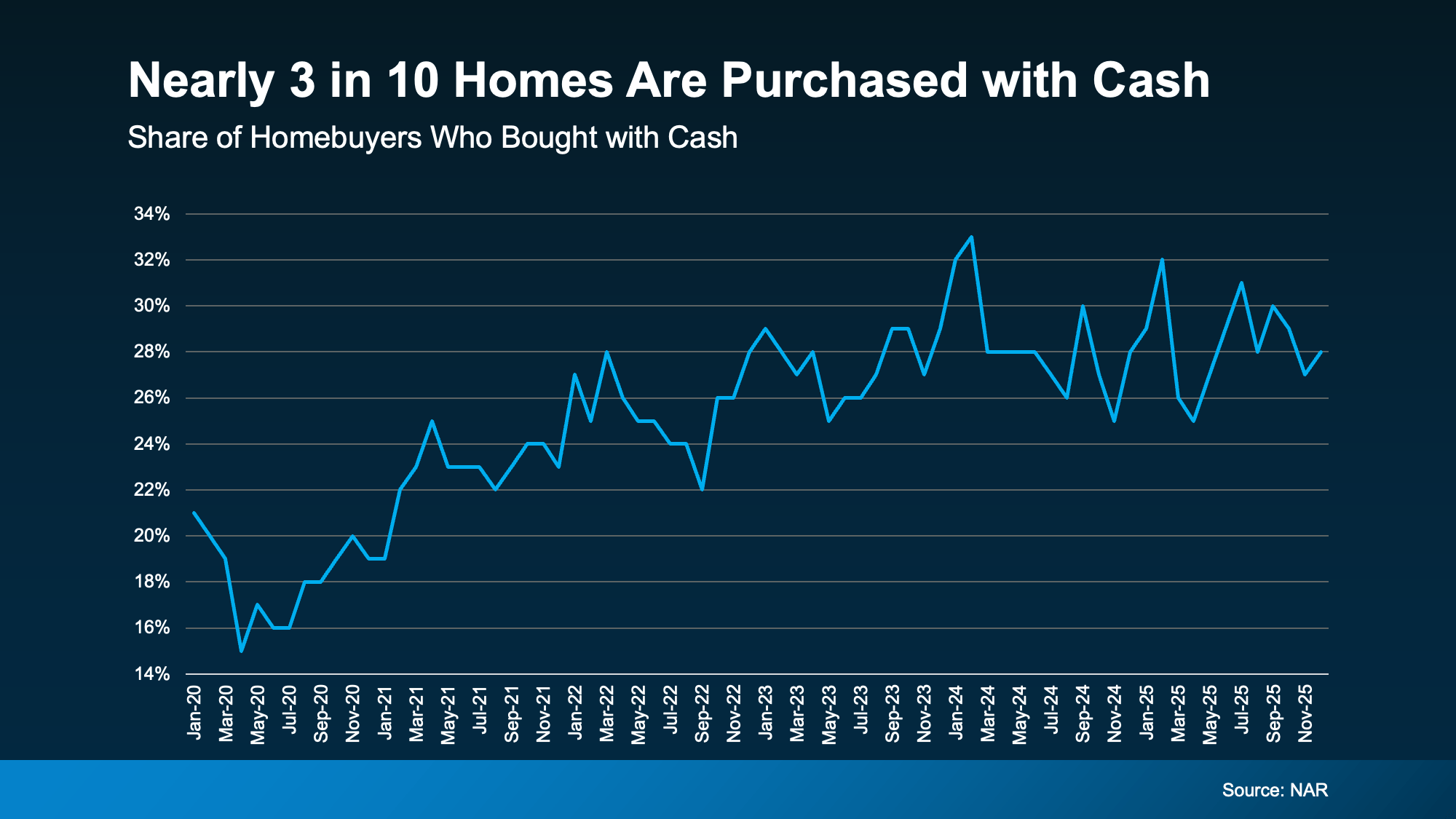

Nearly 3 in 10 homes purchased today are bought in cash, according to the National Association of Realtors (NAR). That’s far more than the pre-pandemic norm (see graph below):

So, how are so many buyers pulling that off? The answer is simple: home equity.

So, how are so many buyers pulling that off? The answer is simple: home equity.

Back in 2020-2021, mortgage rates and the number of homes for sale were both at all-time lows. And that combination pushed home prices up, fast.

If you owned a home during that time, it likely gained significant value – maybe even enough to buy your next house in cash. NAR explains:

“. . . rising home equity has armed many existing homeowners with the financial leverage to make cash offers, allowing them to convert years of price appreciation into immediate purchasing power.”

Here’s why you may want to go that route yourself, if you have enough equity to do it.

1. Your Offer Becomes More Attractive

Sellers value certainty. And an all-cash offer removes one of the biggest unknowns in a transaction: financing. As Rocket Mortgage explains:

“Cash offers are attractive to sellers. Sellers often prefer to work with cash buyers if they can because they don’t have to worry about a buyer’s financing falling through at the last minute.”

In many markets, an all-cash offer can give you a serious edge.

2. You Can Close Faster

And since you don't have to worry about underwriting, lender approvals, and loan processing, the time it takes to close shrinks. Cotality puts it this way:

“Cash buyers have always enjoyed an edge over borrowers. They remove financing risk, reduce delays, and often close in days rather than weeks.”

If the owner of the house you're buying is already under contract on their next home or they just need to move fast (like for a new job), that speed is a real draw.

3. You Won't Have Monthly Mortgage Payments

When you buy in cash, you don’t have to finance your purchase. That means you don’t have to worry about what today’s mortgage rates are and you own the house outright from the day you close. And that’s a big deal.

No mortgage.

No monthly payment.

Full ownership.

That financial freedom opens the door for other big lifestyle benefits. Zillow explains:

“Paying in cash means you own your home outright. This eliminates the need for monthly mortgage payments, freeing up your finances for other priorities like savings, travel, or home improvements.”

4. You May Get a Better Deal

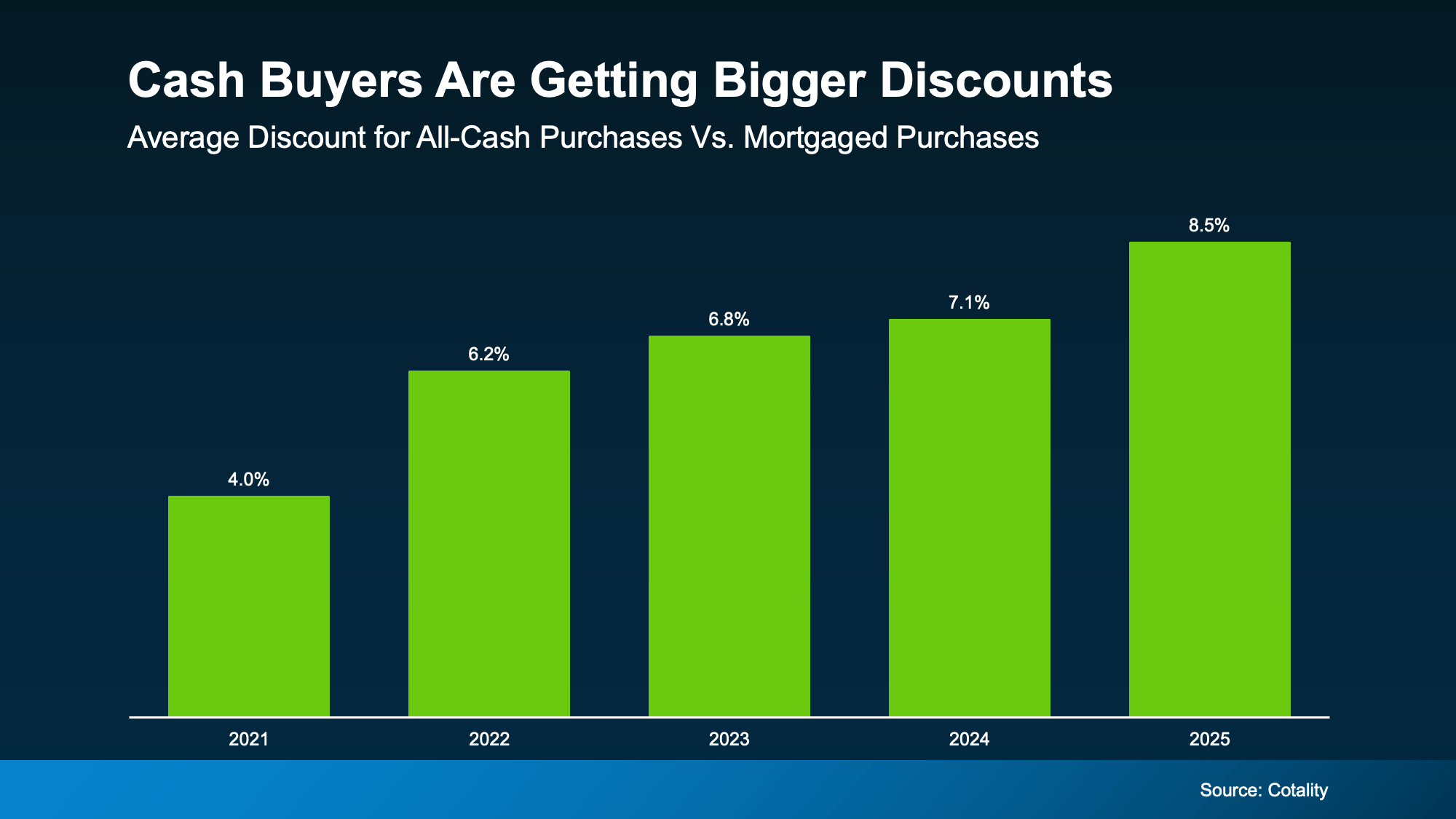

And here’s one more thing that surprises a lot of homeowners: cash buyers often pay less for the house.

According to Cotality, all-cash buyers tend to spend roughly 9% less on the house than buyers who use a mortgage. That’s because some sellers are willing to accept lower offers to get a deal done quickly, with more certainty of closing, and fewer financing hoops to jump through. As Cotality explains:

“From a seller’s point of view, a lower but reliable offer can feel preferable to a higher one that may collapse weeks later.”

And that advantage grows with each passing year (see graph below):

Is an All-Cash Move Realistic for You?

Is an All-Cash Move Realistic for You?

Not every homeowner will buy their next house outright in cash. And that’s okay.

But the bigger takeaway is this: the equity you’ve built may give you more options than you think.

Whether that means downsizing and eliminating a mortgage entirely, or just relocating with stronger negotiating power, your current house may be what makes it possible.

Bottom Line

Before assuming you’ll need another traditional mortgage, it’s worth asking one simple question: How much equity do you really have? Because the answer might change what you thought your next move could look like.

Curious what your home equity could do for you? Ask a local real estate agent to run the numbers and see what kind of buying power you’re really sitting on.

]]>Let’s be clear: selling your house is absolutely possible right now. According to the National Association of Realtors (NAR), roughly 11k homes sell every day in this country.

]]>Let’s be clear: selling your house is absolutely possible right now. According to the National Association of Realtors (NAR), roughly 11k homes sell every day in this country.

And the sellers who are making their moves happen all have one thing in common: they’ve adjusted their strategy to match today’s market. They’re realizing inventory has grown. Homebuyers are more selective. And buyer expectations are higher.

The sellers who struggle are usually approaching today’s market with yesterday’s expectations. Here are the three biggest mistakes they're making – and how to avoid them.

1. Pricing Based on What Their Neighbor Got a Few Years Back

Setting your price is the most important decision you make when you sell – and the one that’s most often mishandled. Realtor.com data shows almost 1 out of 5 sellers in 2025 had to drop their price. Here’s what those sellers went wrong.

Buyers have more choice and more negotiating power now that inventory has grown. And house hunters will actively avoid your house is if feels like it’s priced too high. That's why overpricing usually leads to:

- Fewer showings

- Less competitive (or lowball) offers

- Longer time on market

And all three of those side effects are things you don’t want to deal with.

What To Do Instead: The good news is the cure is simple. Just price for today’s buyer, not yesterday’s headlines. Lean on your agent’s knowledge of recent comparable sales, current competition, and local buyer behavior to land in the value “sweet spot” that drives traffic and urgency from day one.

2. Trying To Skip Repairs That Buyers Now Expect

A few years ago, you could sell as-is and still get well above asking. Today? Not so much. Right now, NAR says two-thirds of sellers are making at least some repairs.

And the reason why is simple. In a market with more inventory, buyers compare homes side by side. Homes that don't show well (or feel dated) are going to lose attention quickly, even if the issues are minor.

What To Do Instead: Ask your agent which high-impact, low-stress updates they’d recommend for your house. The goal isn’t perfection. It’s helping buyers see themselves moving in without a mental to-do list. Small investments in staging, repairs, and curb appeal can make a huge difference in how quickly offers come in – and how strong those offers are.

3. Playing Hardball When Buyers Try To Negotiate

Today’s buyers have housing affordability at the top of their minds. And since money is already tight, they’ll be pickier and will probably ask for some compromises from you. Whether that’s making repairs, giving them a credit at closing, or taking just a few thousand dollars off your asking price, negotiating is normal again.

So, if something pops up in the inspection, you’re going to need to be open to talking about it. If you’re not, you may very well see your buyer walk away. And some sellers are figuring this out the hard way. Redfin data shows one of the big reasons home sales fell thru in 2025 was inspection or repair issues. Odds are those homeowners weren’t willing to flex a bit to get the deal done.

What to Do Instead: Meet with your agent to make sure you understand what buyers in your area care the most about. Align your price with value, present the home clearly and confidently, and stay open to reasonable negotiations that keep deals moving forward.

Bottom Line

The sellers who succeed in this market aren’t doing anything extreme. They’re pricing their house right, making strategic repairs, getting local guidance, and making decisions based on how buyers actually behave today. Those small but mighty mindset shifts could make or break your sale.

Want a real plan tailored to your home and your neighborhood? Talk to a local agent.

]]>Renting can feel like the easier choice right now.

]]>Renting can feel like the easier choice right now. There’s no big down payment. No dealing with surprise repairs. And no long-term commitment.

But then your rent goes up again. And again. And suddenly the thing that seemed flexible starts looking… expensive, especially considering you’re not building any equity. And once that happens, it’s easy to feel a little trapped in the cycle.

That’s because there’s so much chatter today about how buying a home isn’t affordable. But the truth is, the math may work out better than you'd expect based on what’s changed recently.

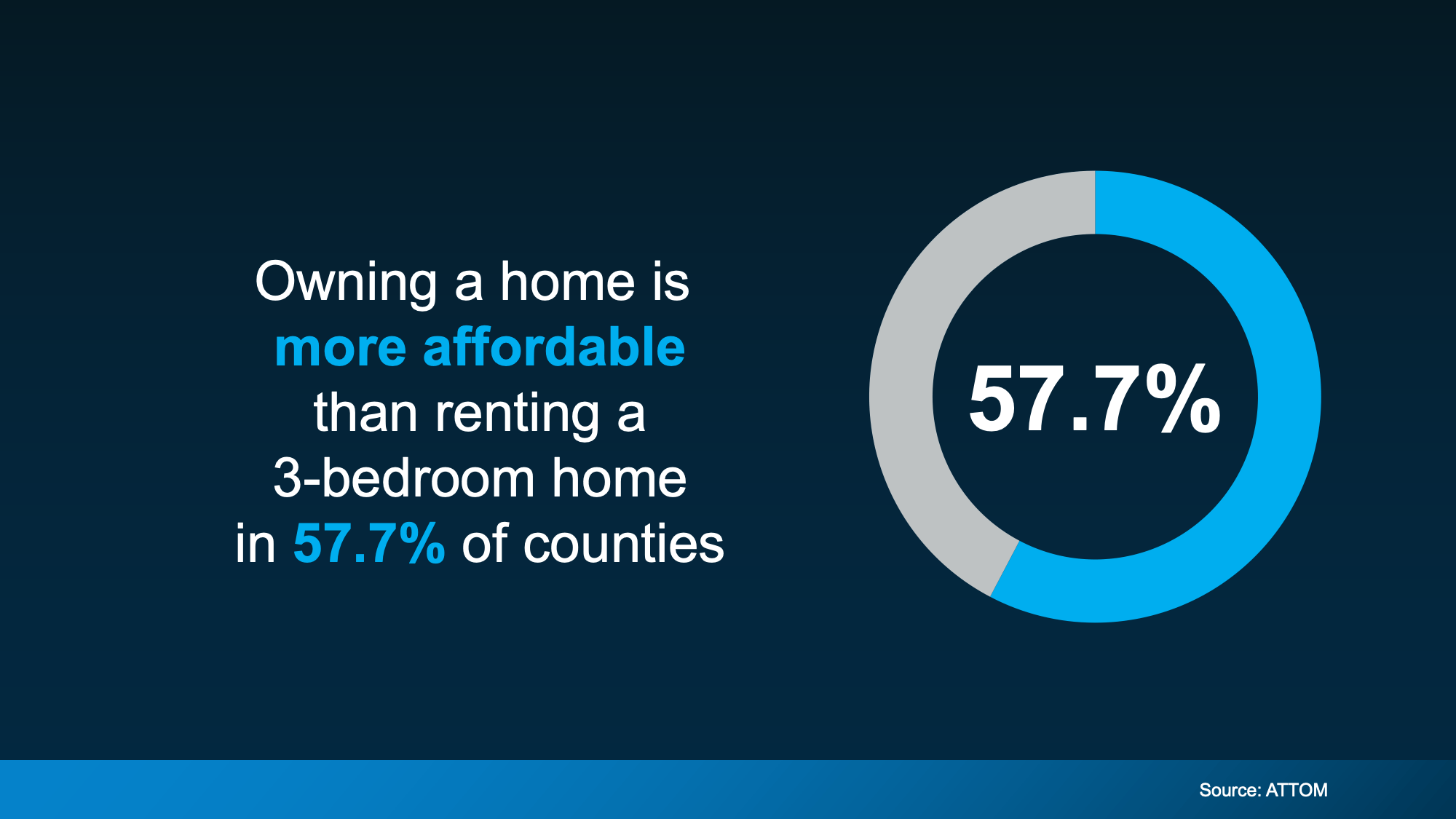

Buying Is More Affordable Than Renting in Many Areas

In a lot of places today, owning a home actually costs less each month than renting a 3-bedroom home. And recent data from ATTOM shows that’s true in nearly 58% of counties across the U.S. (see chart below).

And that's after you factor in things like insurance and typical maintenance costs.

In other words, even though it may feel like a bit of a shock, the numbers show rent often stretches monthly budgets more than owning does. That’s thanks to slower home price growth, more homes for sale, and monthly mortgage payments starting to ease as rates come down.

In other words, even though it may feel like a bit of a shock, the numbers show rent often stretches monthly budgets more than owning does. That’s thanks to slower home price growth, more homes for sale, and monthly mortgage payments starting to ease as rates come down.

Affordability Still Varies by Region

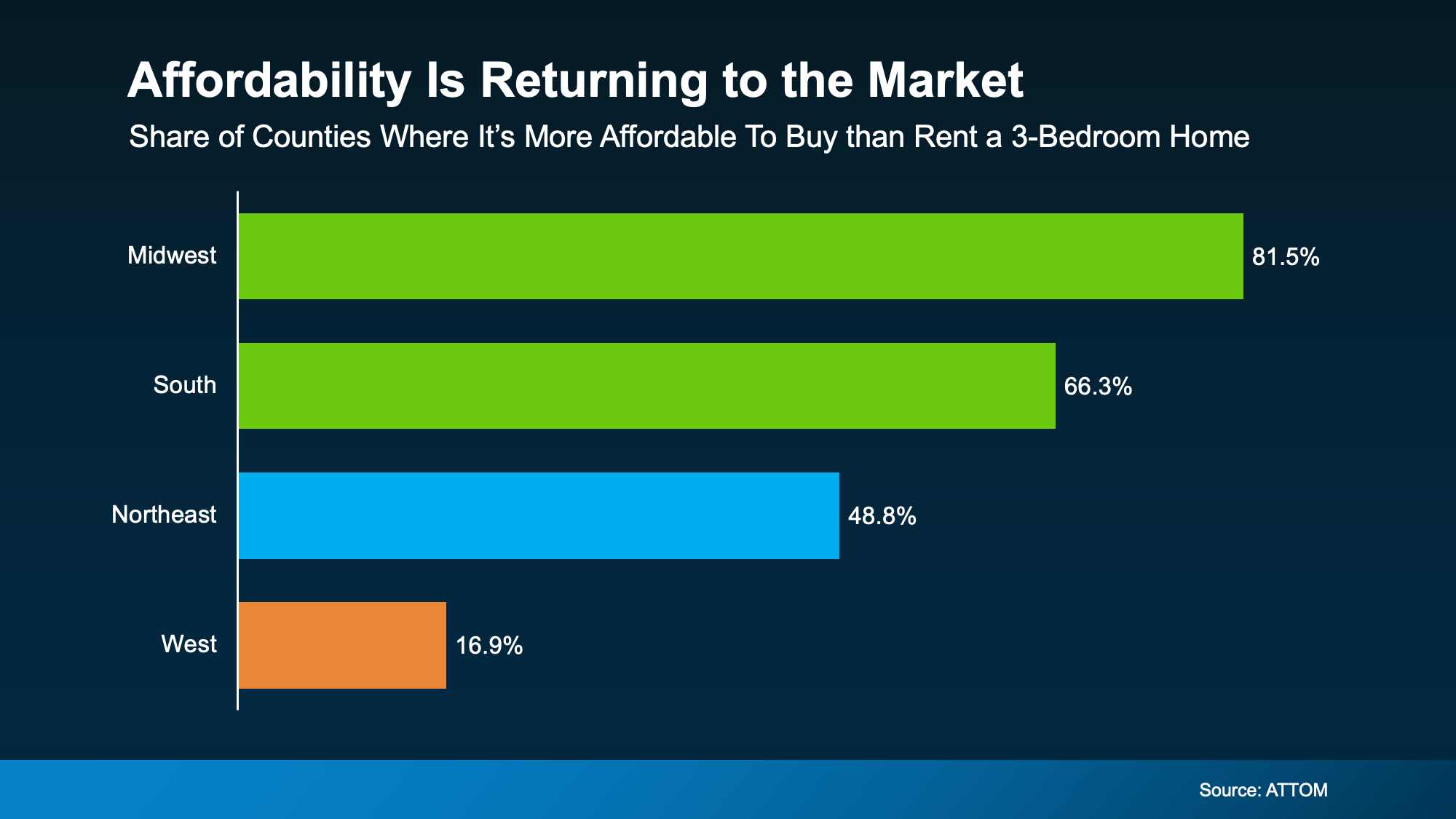

Now, even though nationally the balance has shifted, that doesn’t mean buying is more affordable in every market or for every renter.

While buying is more affordable than renting in nearly 58% of counties nationwide, that share looks different depending on your region (see graph below):

The biggest improvement is happening in the Midwest and South. But if you’re living in the West, things could still feel tight.

The takeaway? How affordable buying is really depends on where you live. And the only way to know how this plays out where you live is to look at the numbers locally.

So, What’s Still Holding Buyers Back?

Maybe you’re nodding along so far but thinking, “Okay, but I still can’t afford the upfront costs.” If that’s your reaction, you’re not the only one.

For many renters, the biggest hurdle isn’t the monthly payment alone. It’s the down payment, too.

But you’re not out of options. Here’s the part most people don’t hear enough about: there are thousands of down payment assistance programs available across the country, and many buyers qualify without realizing it.

And the average benefit? Roughly $18,000.

That kind of support can help cover part of your down payment or closing costs, which means you may not need to save nearly as much as you think to get started.

When you combine that with monthly payments that may work better than expected, especially as rates continue to ease and prices cool, buying may feel far more realistic than it looks at first glance.

Bottom Line

The point isn’t that everyone should rush out and buy a home tomorrow.

It’s that renting isn’t always the more affordable option people assume it is – and buying may be more realistic than it feels once you look at the full picture.

If you’re renting and feeling stuck in the “someday” loop, it might be worth a simple conversation with a local real estate agent or lender. Just a chance to see what’s possible and whether it makes sense for you.

]]>